Search

close

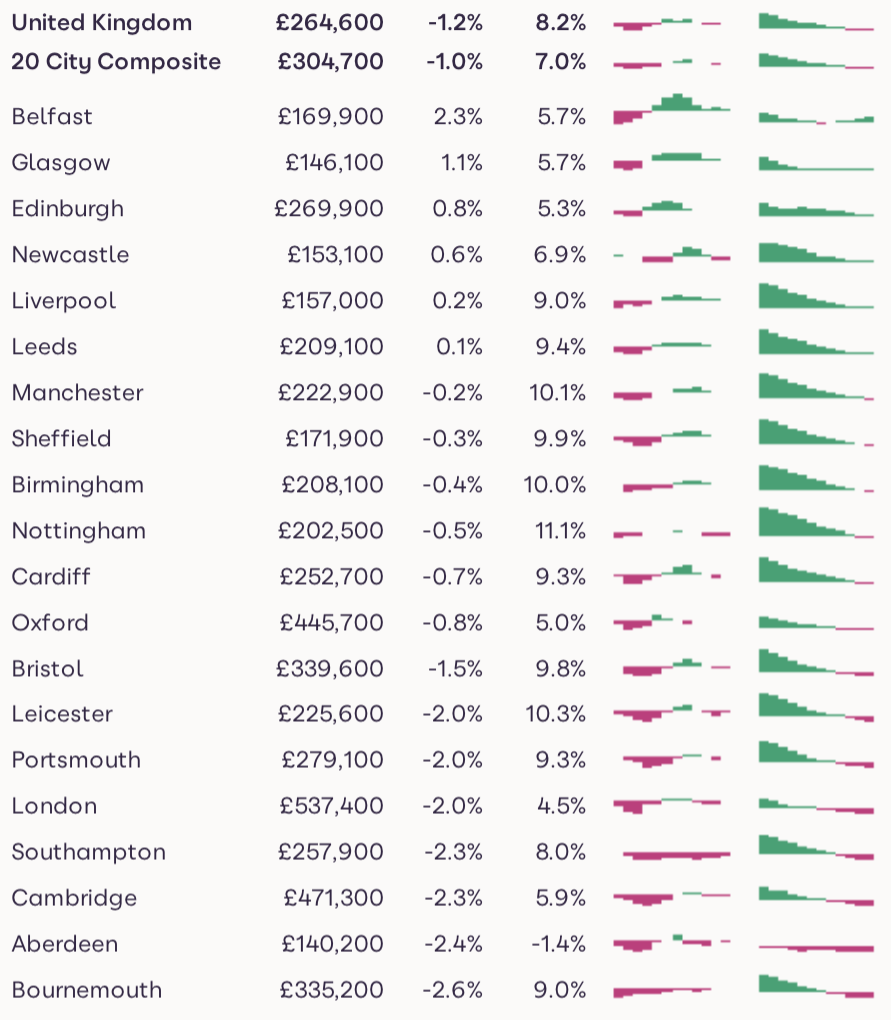

Homebuyers are largely shrugging off the election with new sales agreed 8% higher, with demand up 6% and a fifth (19%) more homes for sale than a year ago.

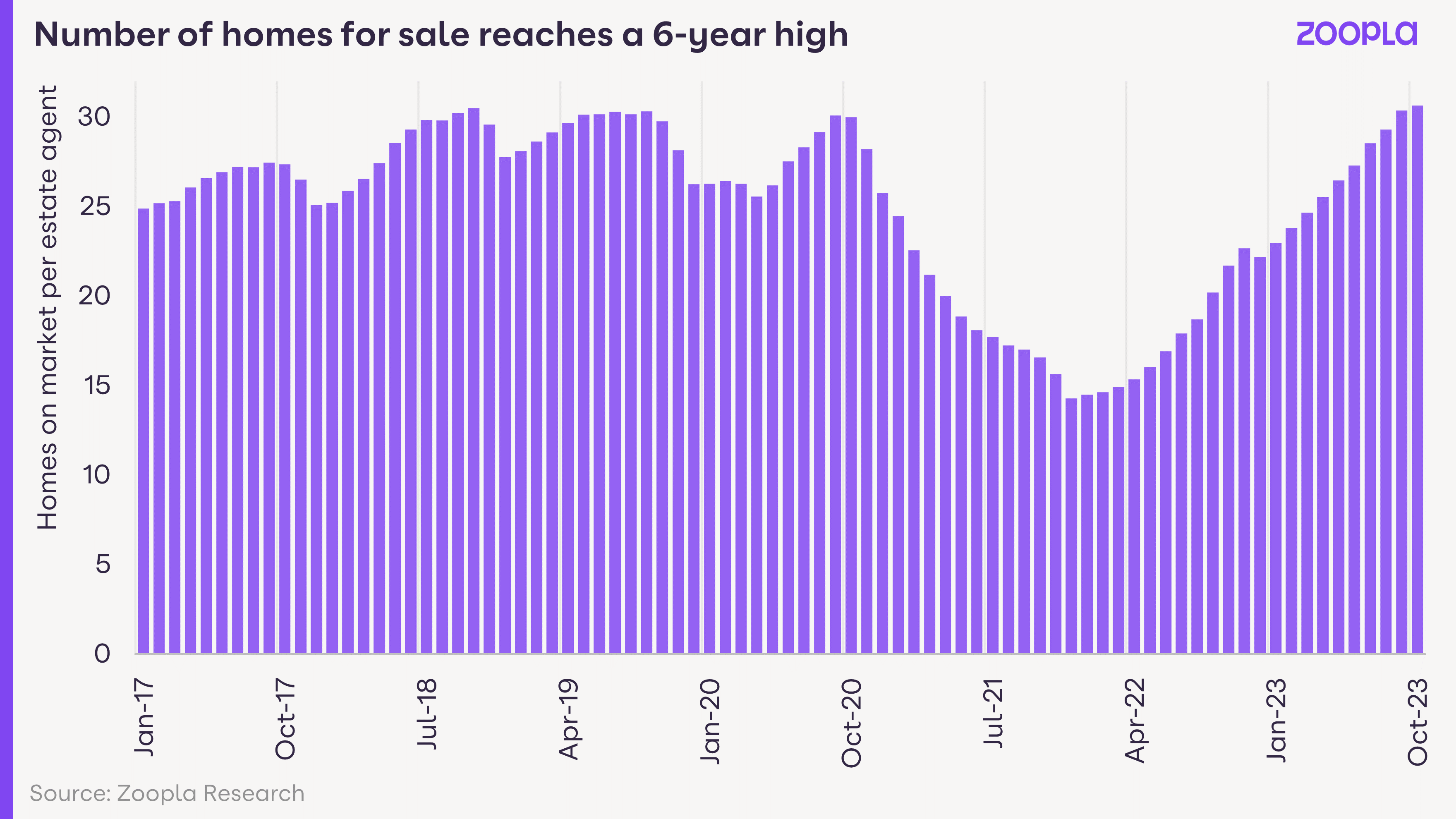

The supply of homes has fully recovered showing greater intent amongst sellers, many of whom are also buyers.

What effect will the general election have on the housing market?

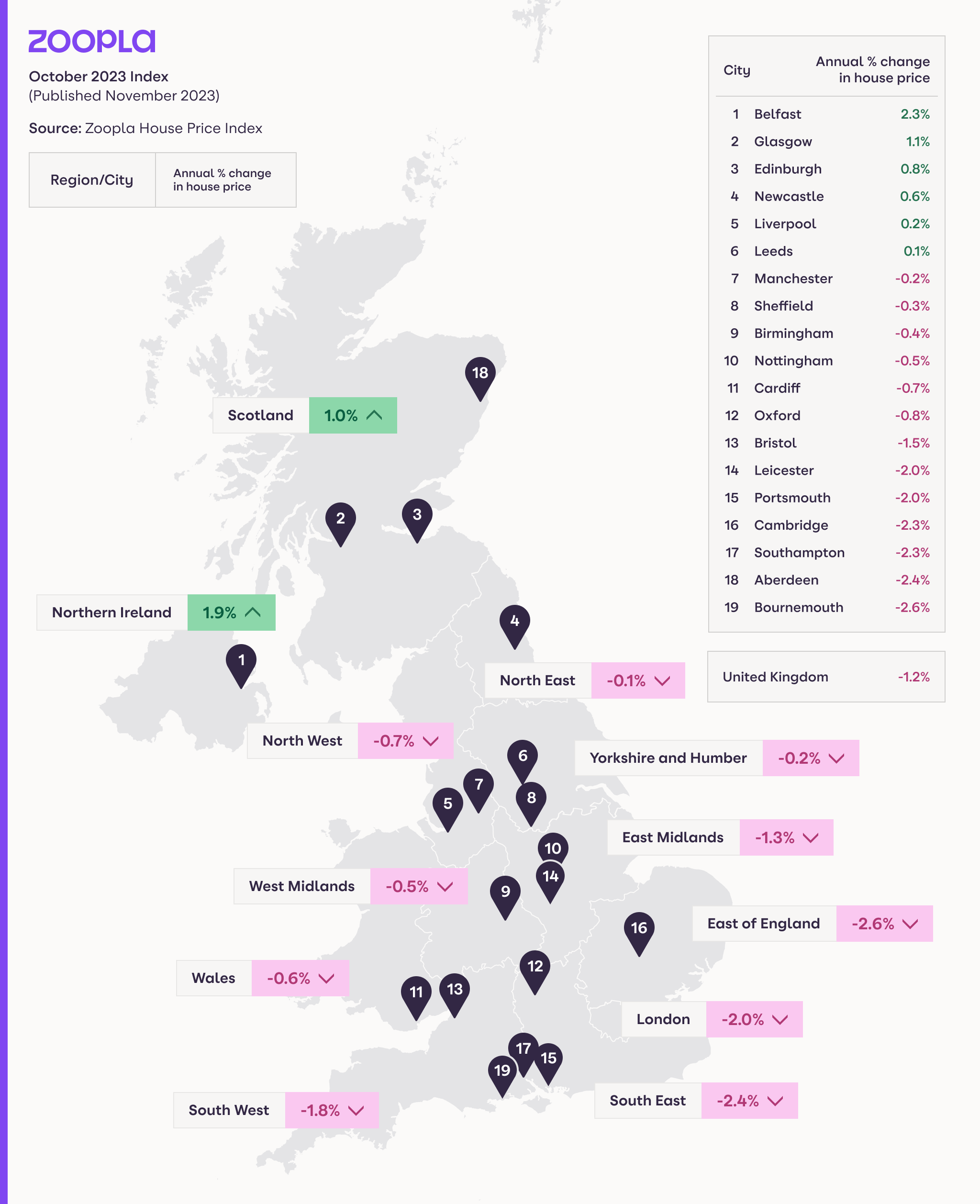

The housing market continues to adjust to higher mortgage rates. Sales volumes are rising and house prices are static.