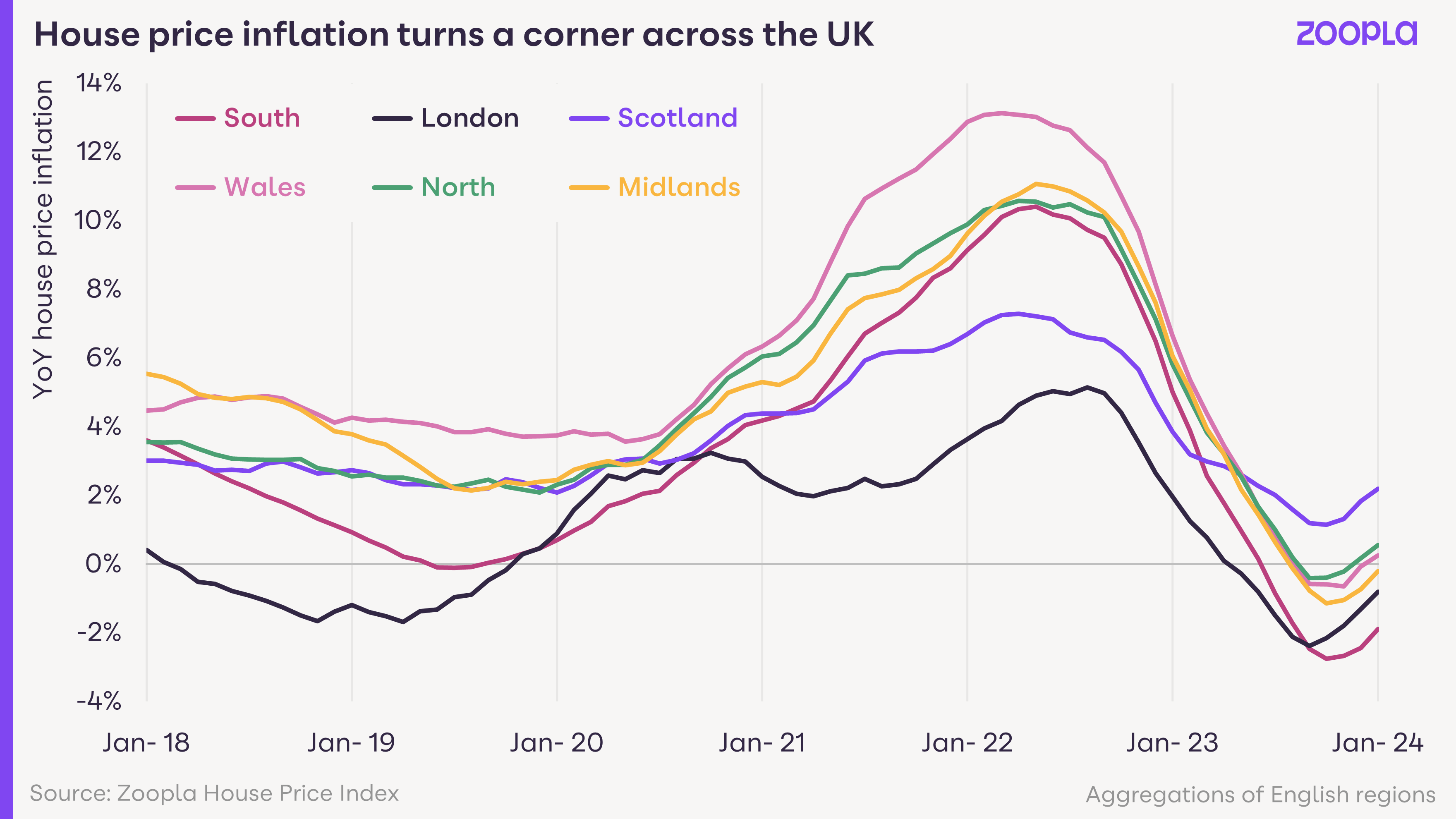

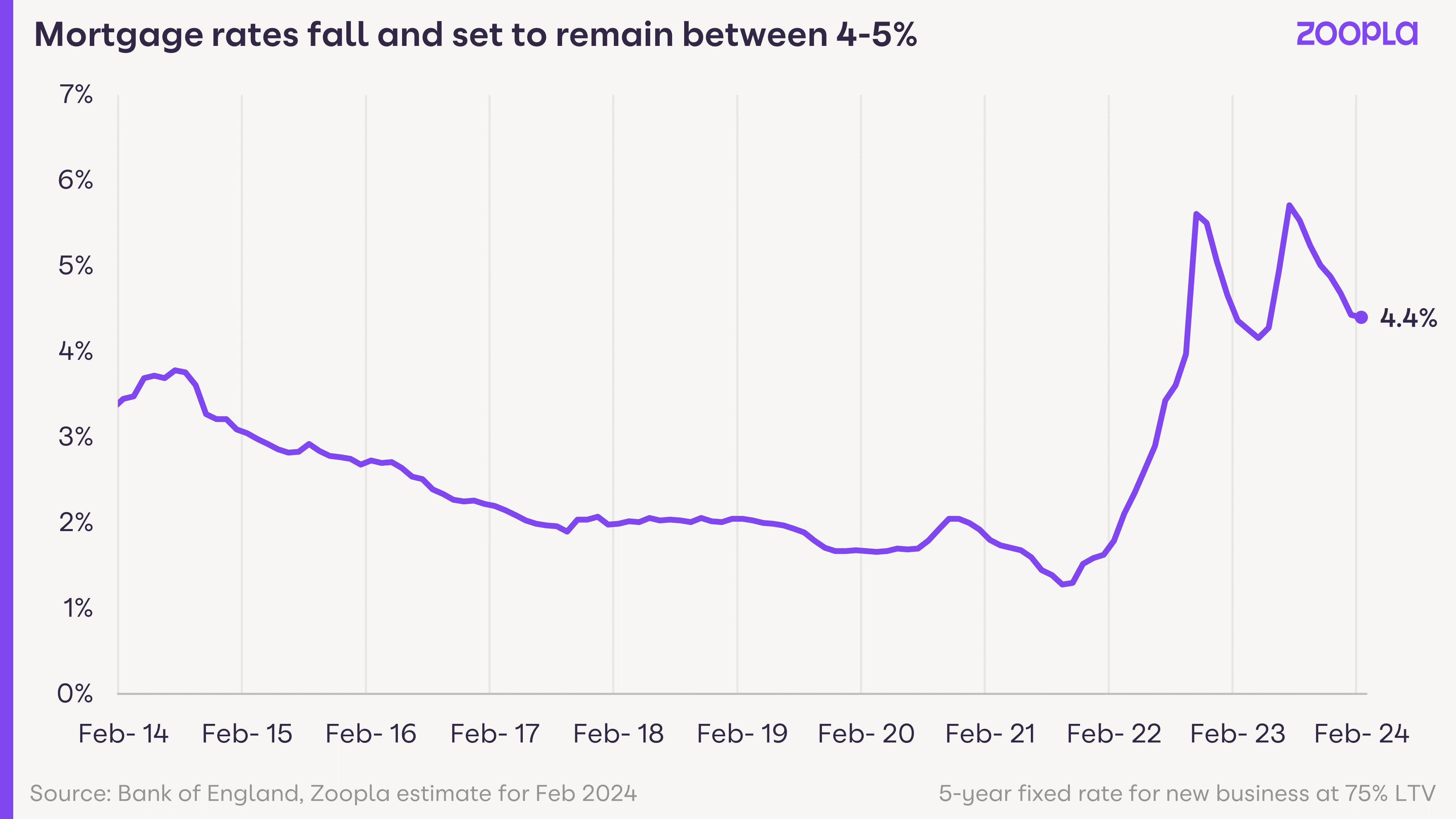

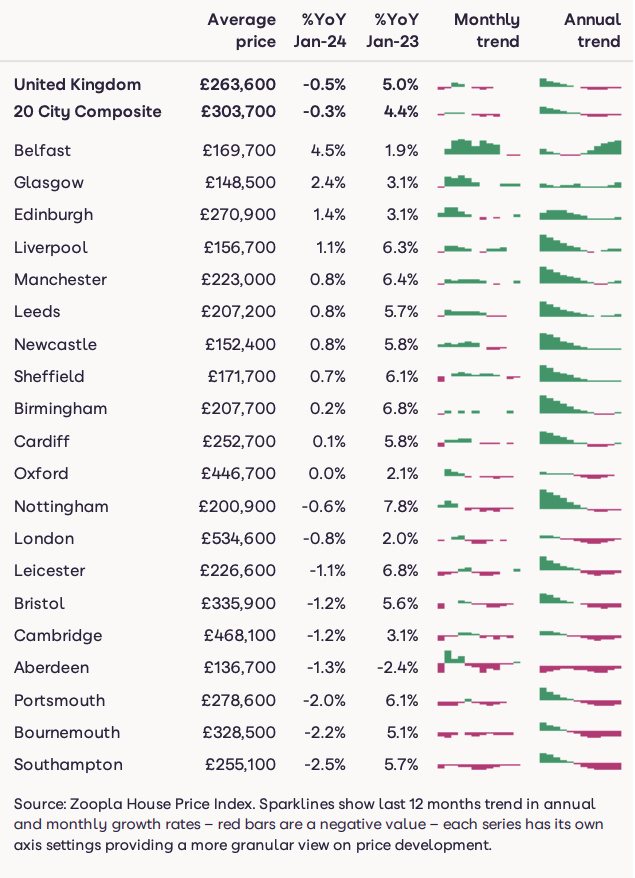

Higher mortgage rates and cost of living pressures have driven a rapid slowdown in the rate of house price inflation over the last 18 months. There are some notable variations in price inflation across the country which are primarily explained by the relative affordability of housing.

Current housing trends fall into one of three groups.

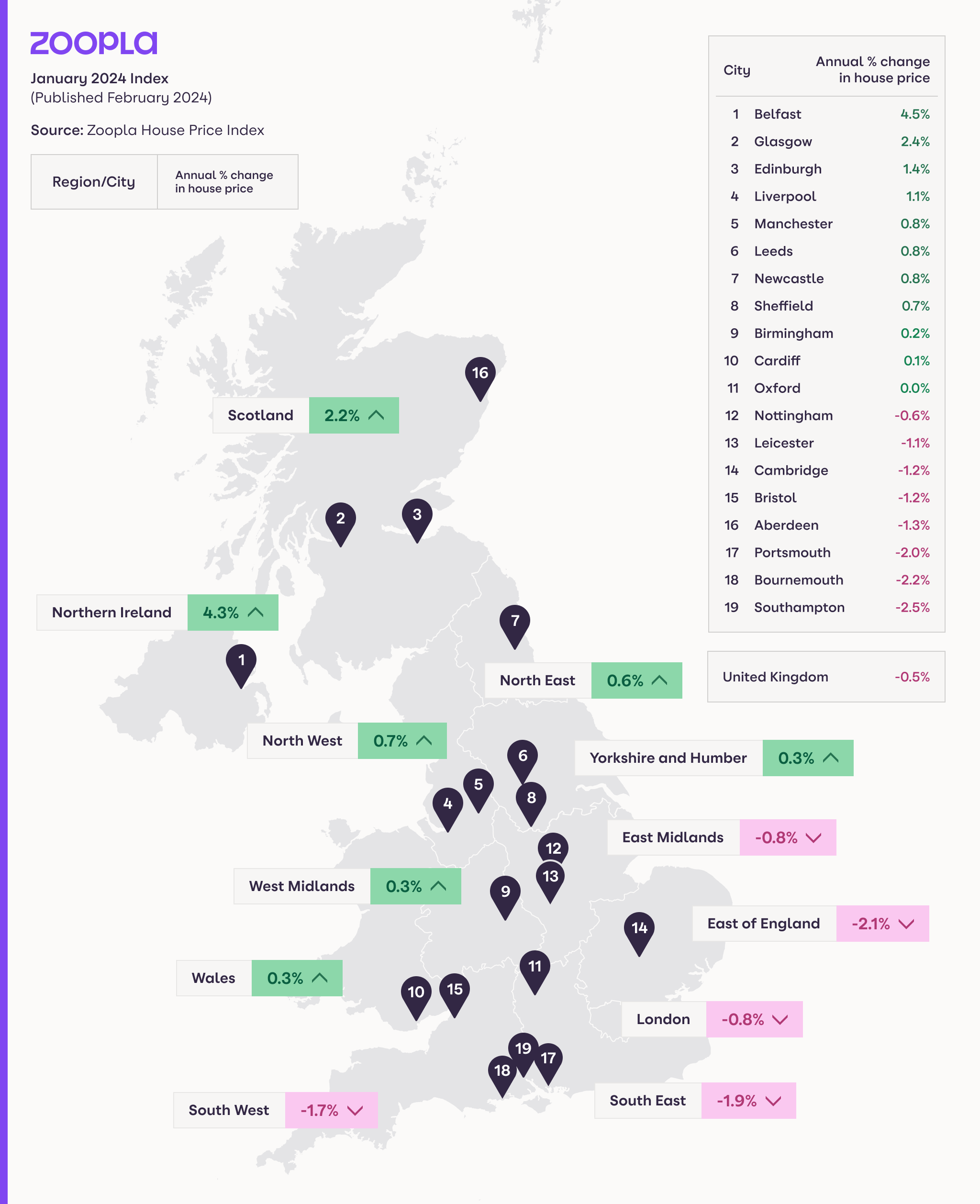

1) Southern England regions – covering East of England, South East and South West regions, these areas have registered the largest annual price falls. Rising mortgage rates and reduced household buying power have hit higher-priced markets harder than more affordable markets. Average home prices are £344,000 in these areas, 30% above the UK average. The pace of price falls is starting to moderate in Southern England, but it’s lagging other areas of the UK.

2) London – we see London differently to the rest of southern England. While it is the most expensive housing market, with an average price of £534,000. almost 2x the UK average. However, weak house price inflation over the last seven years has improved affordability and opening the market up to more potential buyers than before.

The rebound in demand and low growth in the supply of homes for sale (just 7% in London vs 21% for the UK) explains why house price inflation is rebounding quicker than the southern England regions.

3) Rest of the UK – while house price growth has slowed rapidly over the last 12 months, annual price falls have been very limited across the rest of the UK where average house prices are 28% below the UK level. This explains why the impact on buying power from higher mortgage rates outside Southern England has been less pronounced.

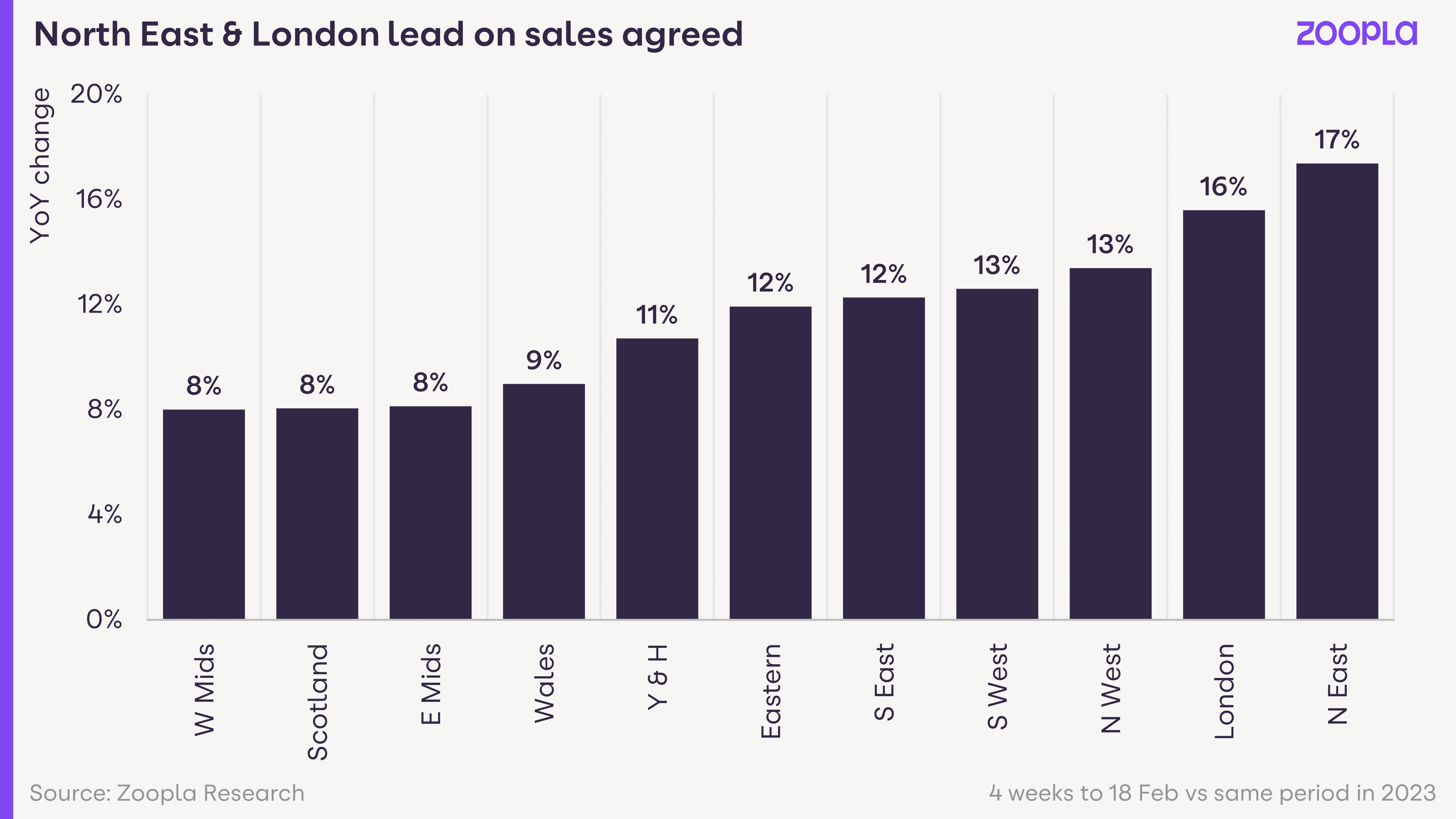

Our index shows Scottish house prices remaining in positive territory over the whole of the last year. Northern regions of England, the West Midlands and Wales are registering firmer pricing in response to rising sales agreed and better levels of housing affordability.