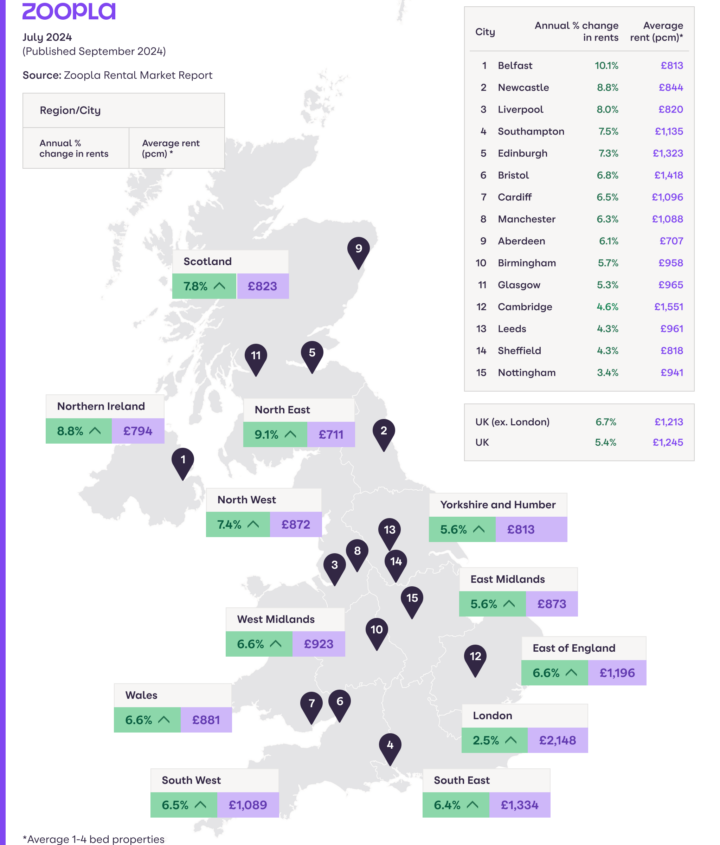

London and other major cities across the UK have been leading the slowdown in rental inflation. The UK’s largest cities have recorded some of the greatest gains in average rents, averaging over 10% per year for the last 3 years. This pace of rent rises is unsustainable and means affordability is starting to impact rental growth.

Segmenting our rental index by type of area shows the greatest slowdown has been in London, where rents are rising at just 2.5% -down from over 12% last year. Rental growth is slowing quickly across the UK’s other largest cities, the so-called ‘core cities’, with rents 5.8% higher over the last year – down from 10.7% a year ago.

Cities are major hubs of rental supply and together London and these 12 core cities account for 30% of all private rented homes (and just 13% of local authorities). The remaining 70% of rented homes are spread across other cities and towns of different sizes.

Rental inflation in these non-city areas continues to run at an above-average rate of 6.8% to 7.4% a year. This reflects demand being pushed into more affordable areas, often adjacent to larger cities which are key employment centres.