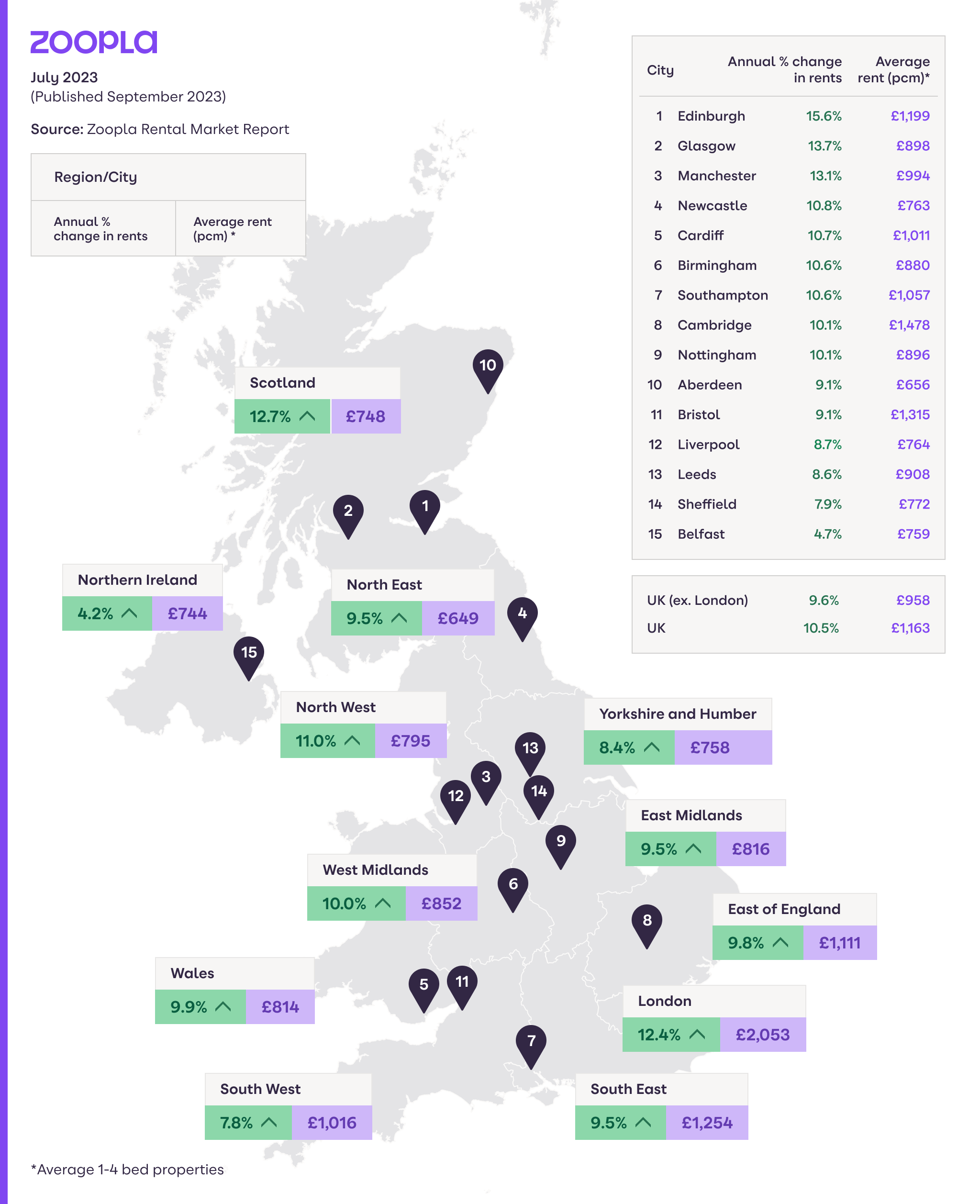

The rental market remains stuck in a period of low supply and high demand. Growing rental supply is the most efficient and sustainable way to reduce rental growth. However, levels of home building and net new investment by private landlords is falling and set to remain weak into 2024 due to the impact of higher borrowing costs.

New investment from corporate landlords via ‘build-to-rent’ is a bright spot, boosting supply in many city centres. However, rental levels set by corporate landlords are above-average and not at a scale to impact the wider market.

Many existing renters will also try to avoid moving and paying a higher rent, delivering a further drag on available supply. The net result is that the average estate agent has less than 10 homes to rent compared to a pre-pandemic average of 16.5 homes.

Demand for rented homes continues to be driven by multiple factors. The strength of the labour market and job creation is a key driver of rental demand, as is record levels of immigration. This was particularly apparent a year ago as international borders re-opened with an influx of overseas students returning to study in the UK. The number of renters chasing each property for rent spiked to a record high over the summer of 2022.

Demand has risen again this year, tracking the seasonal trend, but is now 20% lower than a year ago. Rental demand is also boosted by higher mortgage rates, which have increased the cost of buying, keeping more would-be buyers in the rented sector.

Mortgage repayments for a first-time buyer are more expensive than rental costs at 5.5% mortgage rates. The greatest impact of this is being seen across southern England.

The net result of these trends is that the current supply/demand imbalance shows no sign of reversing as we move into 2024. Rental growth in the near term is set to be shaped more by the affordability of renting, and how renters adapt to higher rents, than major shifts in supply and/or demand.