Rental demand has cooled across all regions and countries of the UK over the last year. This is largely a result of lower levels of immigration for work and study, as well as greater first-time buyer demand, most of whom originate from the rental market.

The average annual cost has risen by £3,000 over the last 3 years, and these growing renting costs are also likely to be suppressing demand for new lets, encouraging renters to stay put for longer to avoid higher costs from moving home which also reduces supply.

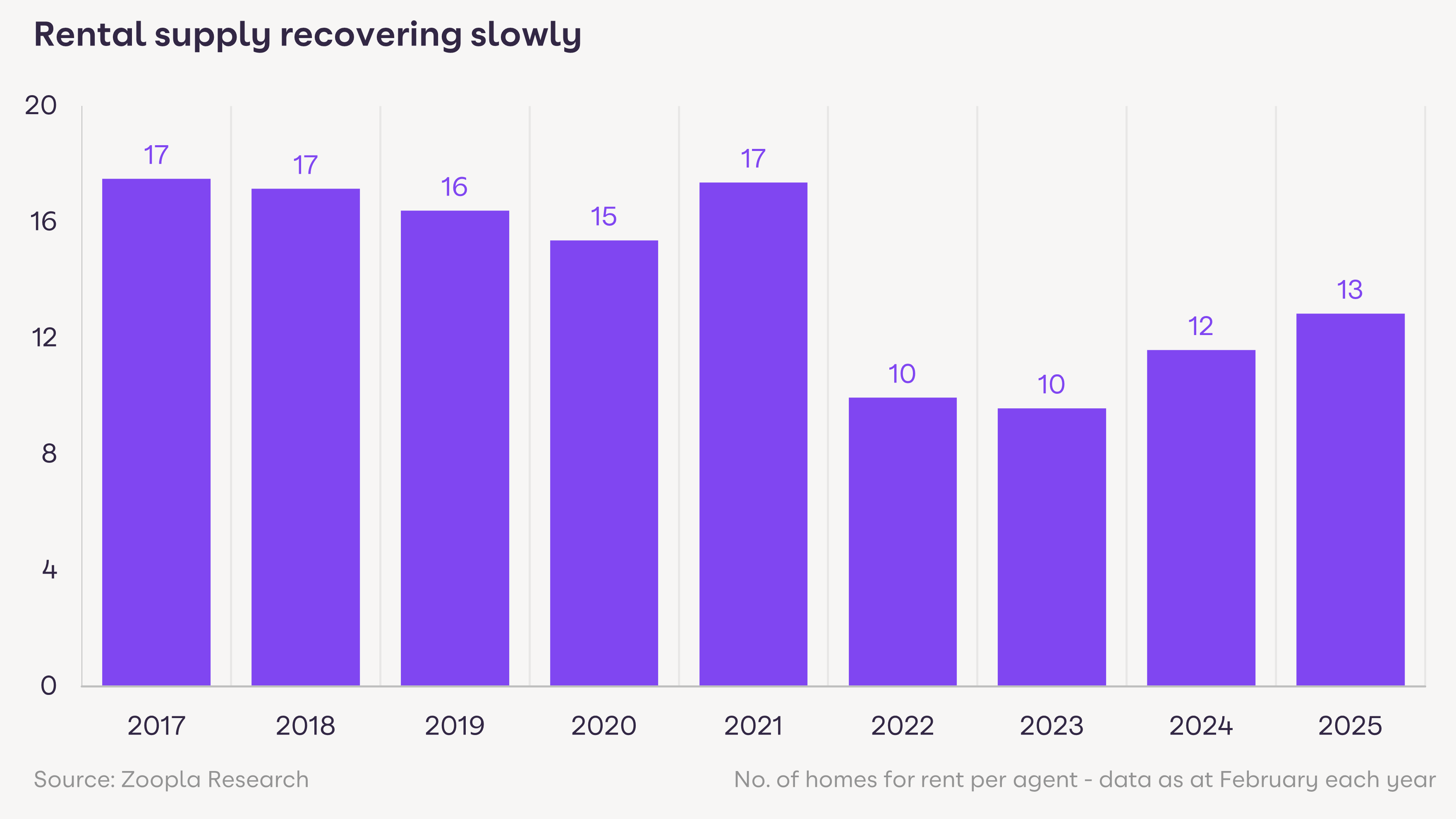

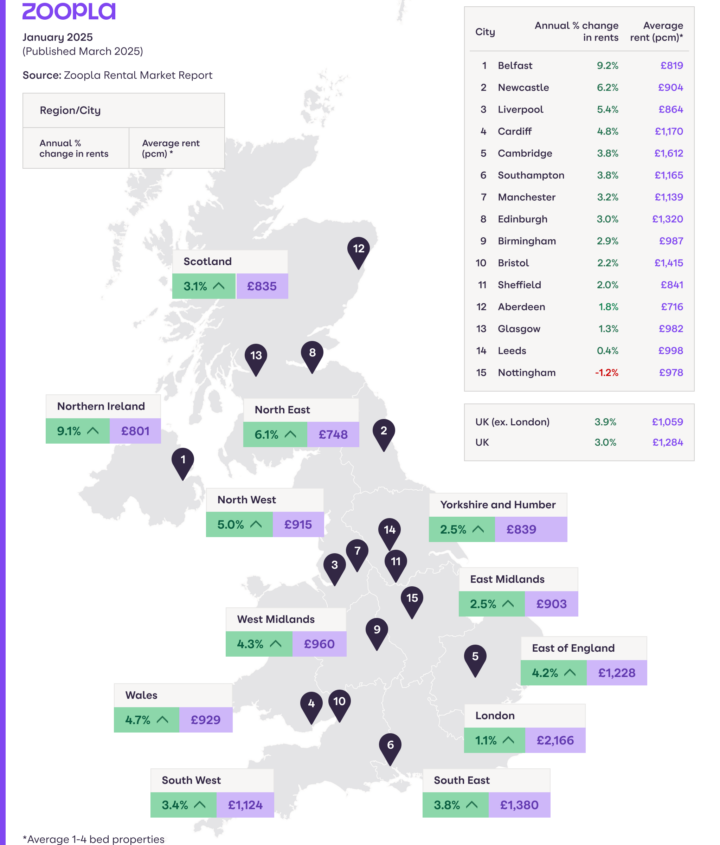

The number of homes for rent has increased in all areas of the UK except in the West Midlands, where supply is 10% lower than last year. The number of homes for rent has grown most in the North East (23%) and Scotland (29%). Rising supply is welcome news for renters, but supply remains below pre-pandemic levels across all areas except for the East Midlands.

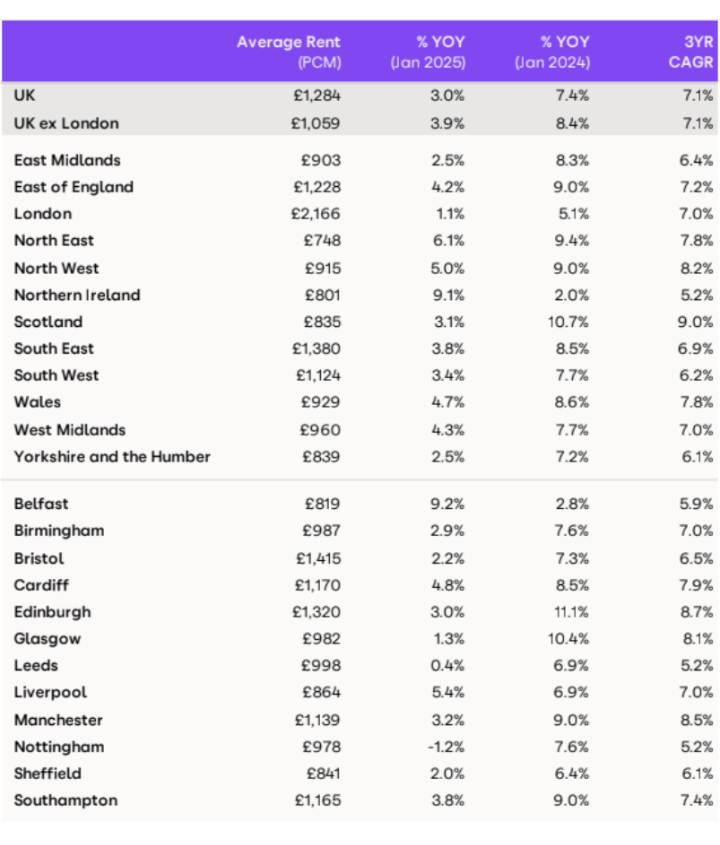

Rental inflation ranges from a low of 1.1% in London to 6.3% in the North East and 9% in Northern Ireland. In addition to London, rental inflation has slowed rapidly in Scotland and the East Midlands over the last year, as the number of homes available to rent increases.