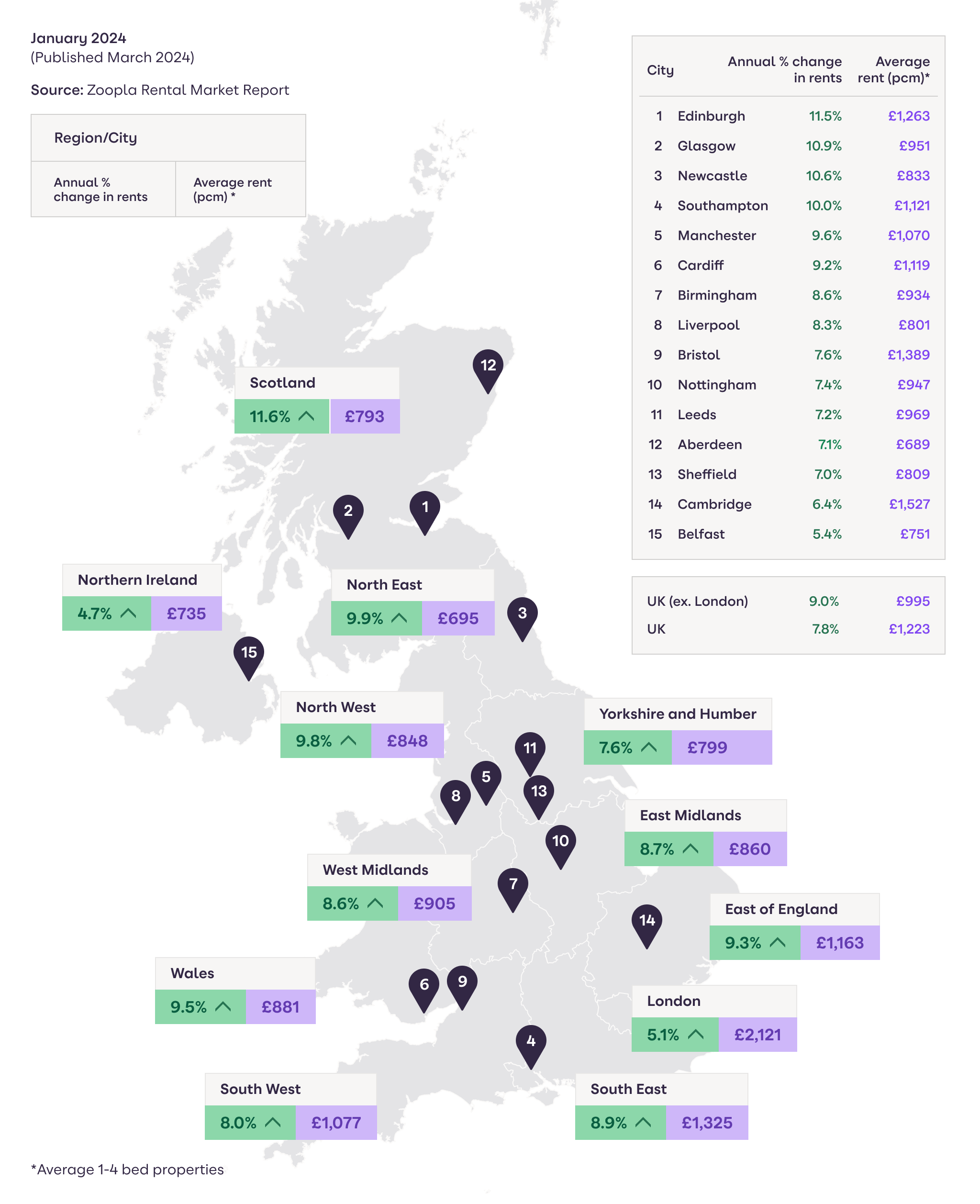

The heat is finally coming out of UK rental inflation which has slowed to 7.8%, down from 11% a year ago – the lowest rate for 2 years. The average UK rent is now £1,223 per month.

The moderation in rental inflation is down to weakening demand and growing affordability pressures, rather than major expansion in supply. Levels of new investment by private landlords remain low.

The average letting agent has now 12 homes for rent – this is a fifth higher than last year but 28% below the pre-pandemic average (16).

Demand for rented homes has fallen by a fifth over the last year as one-off pandemic factors recede, the labour market cools, and lower mortgage rates support first-time buyers.

However, there remain more than 15 enquires for every home for rent – this is down from over 40 enquiries in 2021 but still double pre-pandemic levels.

The supply/demand imbalance is narrowing but is far from closed. Rents will continue to rise over 2024, albeit at a slowing rate.