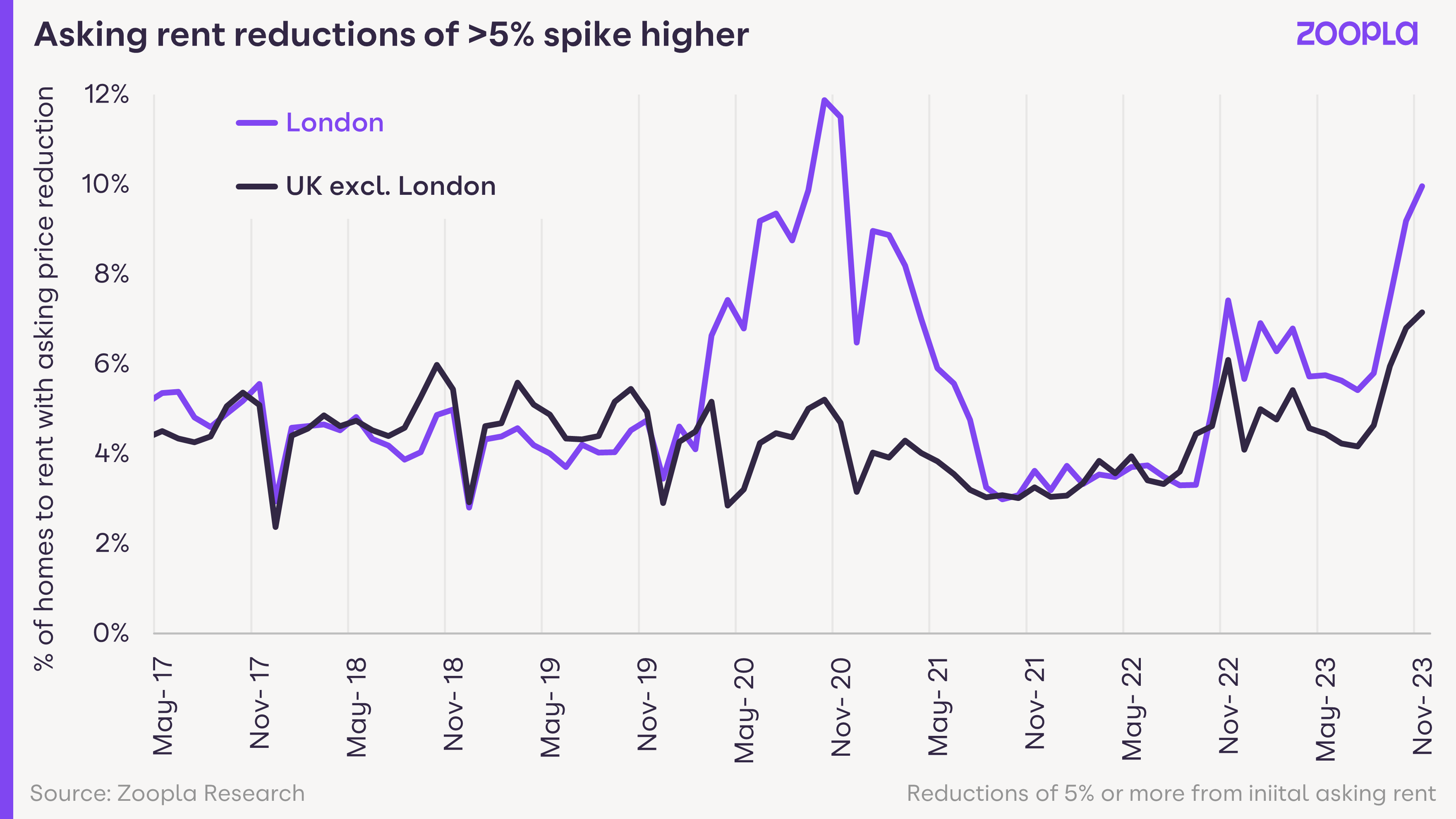

One important indicator of underlying demand, and the impetus for rental growth, is the extent to which asking rents for rental listings are being reduced to attract more applicants.

Asking rent reductions of over 5% at a national level are currently tracking in line with the second half of 2020 when the pandemic hit demand, supply expanded, anc rental growth slowed.

The volume of asking rent reductions of over 5% is currently the highest in London. 10% of rental listings in November 2023 were impacted. Meanwhile, the proportion across the rest of the UK has also jumped to 7%, the highest it has been for over 5 years.

This is evidence that the strong upward momentum in rents over the last 3 years is meeting some resistance as renters face growing affordability pressures and earnings growth starts to moderate.

These reductions are evenly spread across the market by rental price band with a concentration in the £1,000-£1,500 per month bracket.