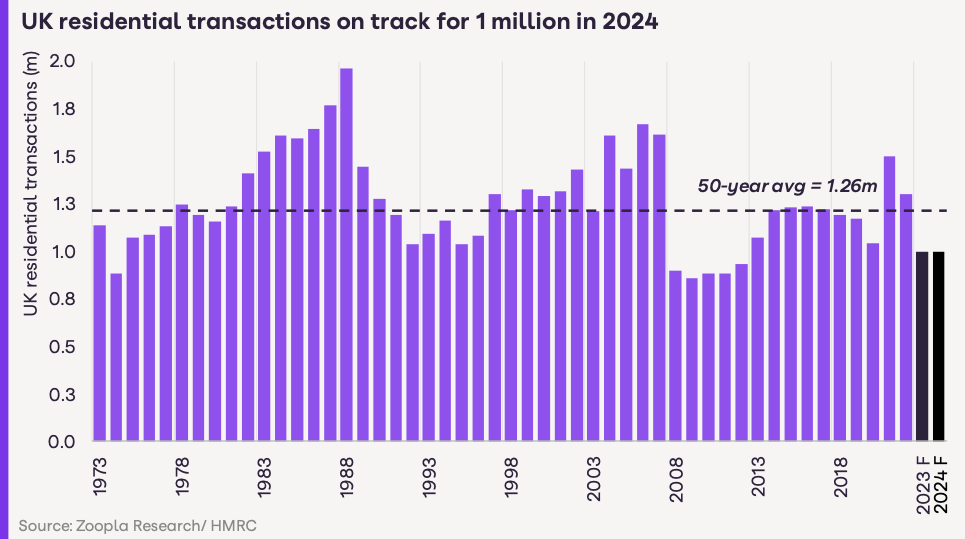

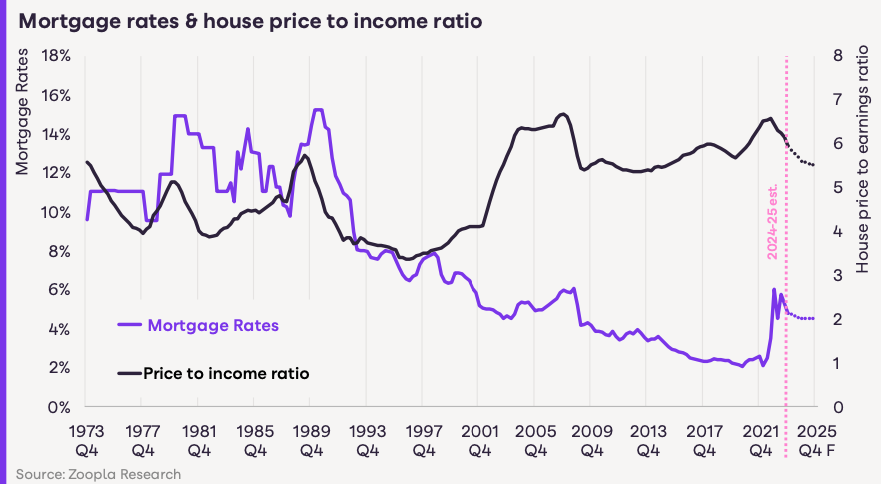

Higher mortgage rates and the cost-of-living squeeze have hit buyer demand. The first half of 2023 registered a rebound in demand as mortgage rates fell towards 4%. A jump in borrowing costs over the summer has reduced demand once again. It is a fifth lower on an annual basis and 25% below the 5-year average for October. The result has been a rapid slowdown in price growth from +9.2% a year ago to -1.1% today. Other indices, based on mortgage lending, have registered larger annual falls, while the ONS’ House Price Index was +0.2% in July.

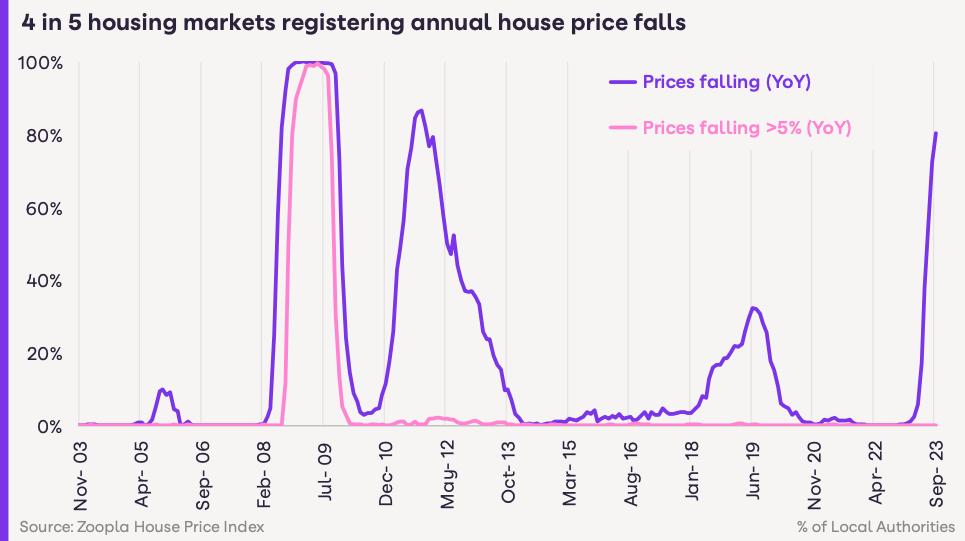

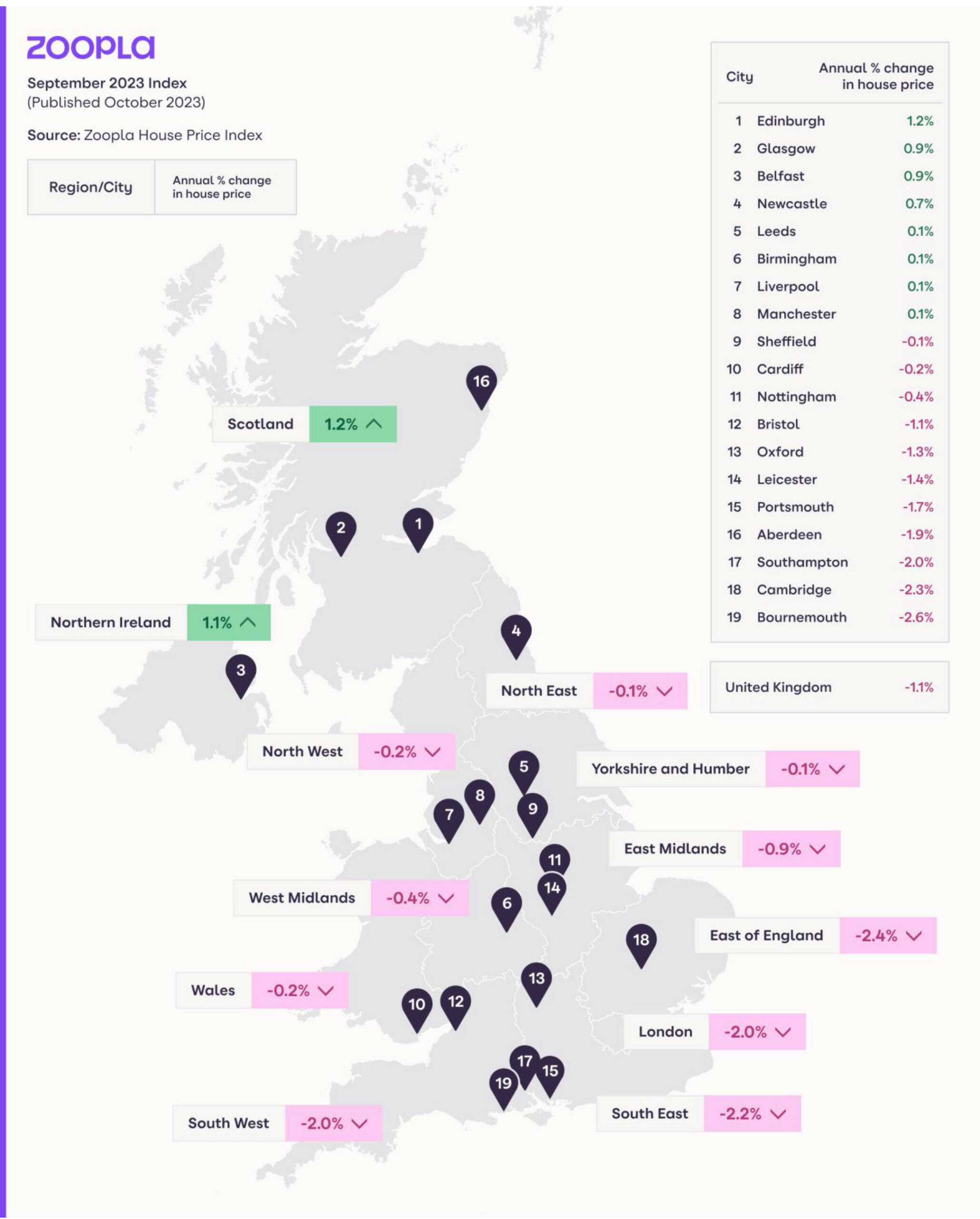

Southern England has been at the forefront of price reductions to date, but these are now spreading further afield. Our localised house price indices1 show that 4 in 5 housing markets are registering annual price falls, up from less than 1 in 20 just six months ago. The scale of price falls is modest, limited to very low single digits. No markets are registering annual price falls over 5%. We expect to start seeing some markets register annual price falls over 5% in the coming months as pricing continues to adjust in the face of weaker buying power.

The largest annual price falls at a larger, postal area level, are recorded in Colchester (CO) where prices are 3.5% lower over the year. This is followed by Canterbury, Luton and Brighton – all London commuter areas. Prices in Halifax (HX) are 3.6% higher than a year ago and 2.4% higher in the Motherwell (ML) postal area in Scotland.