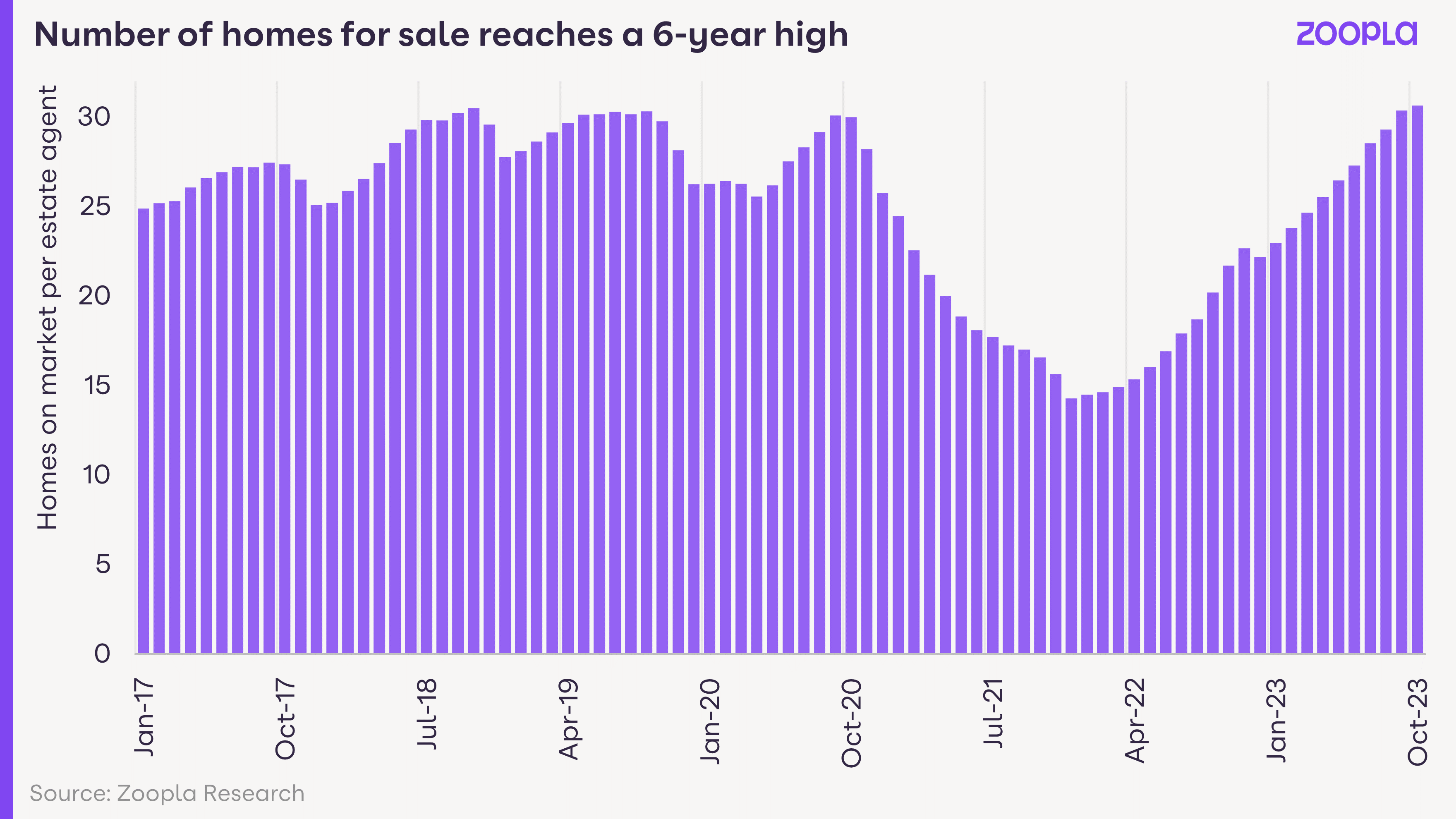

Buyer demand weakened over the summer as mortgage rates increased. While there has been a modest rebound over the autumn, demand remains 13% lower than 2019. Demand is also 10% higher than last year when the fallout from the mini budget drove a rapid decline in buyer interest.

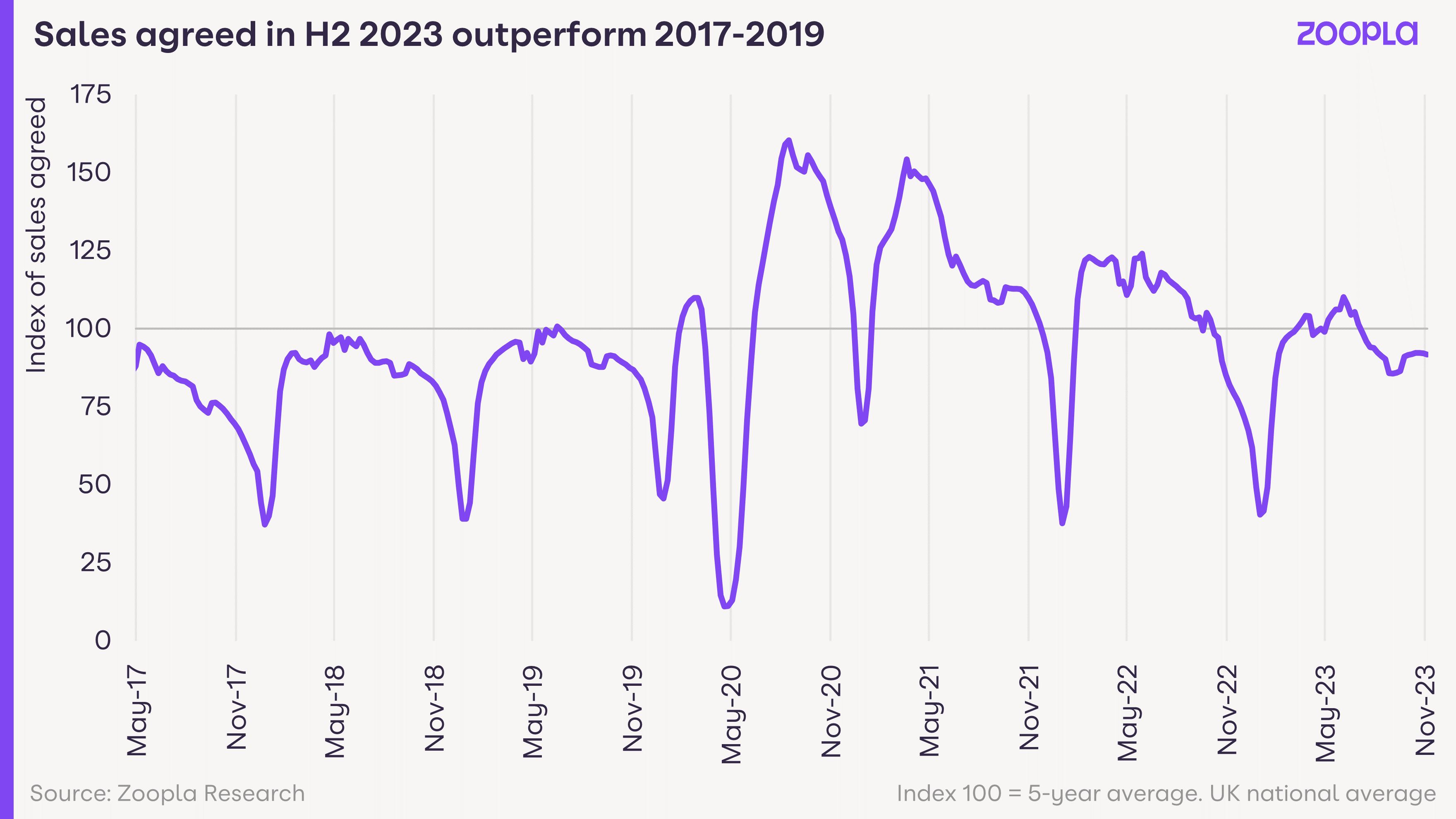

While there are fewer buyers in the market, new sales are still being agreed, tracking 15% higher than a year ago and 5% higher than 2019 levels. This indicates greater realism on the part of sellers and a growing sense that mortgage rates may have peaked and could start to fall later in 2024. It is encouraging those who have delayed decisions to commit to new agreeing purchases, especially if there are better deals to be had from a stronger negotiating position.

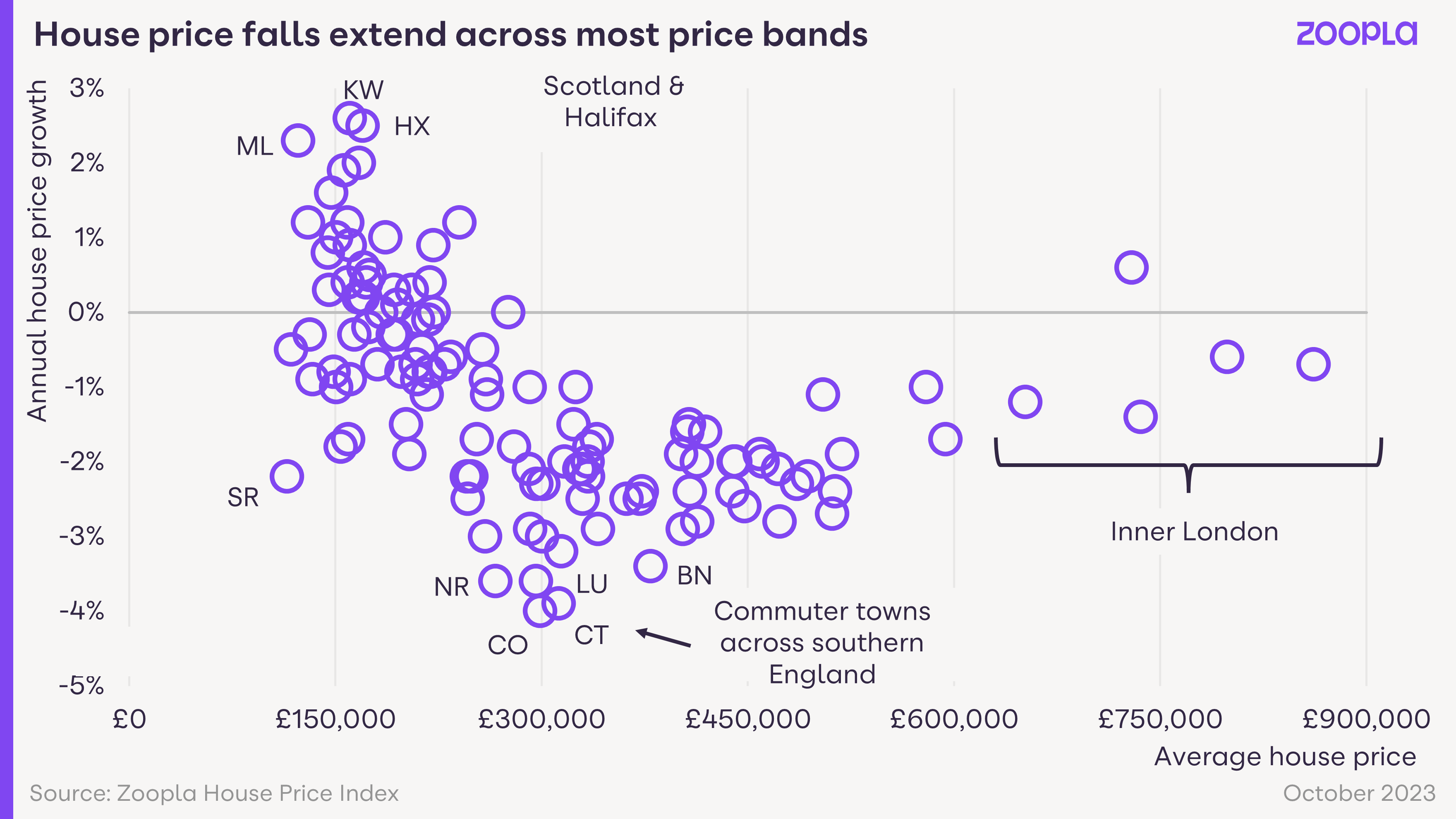

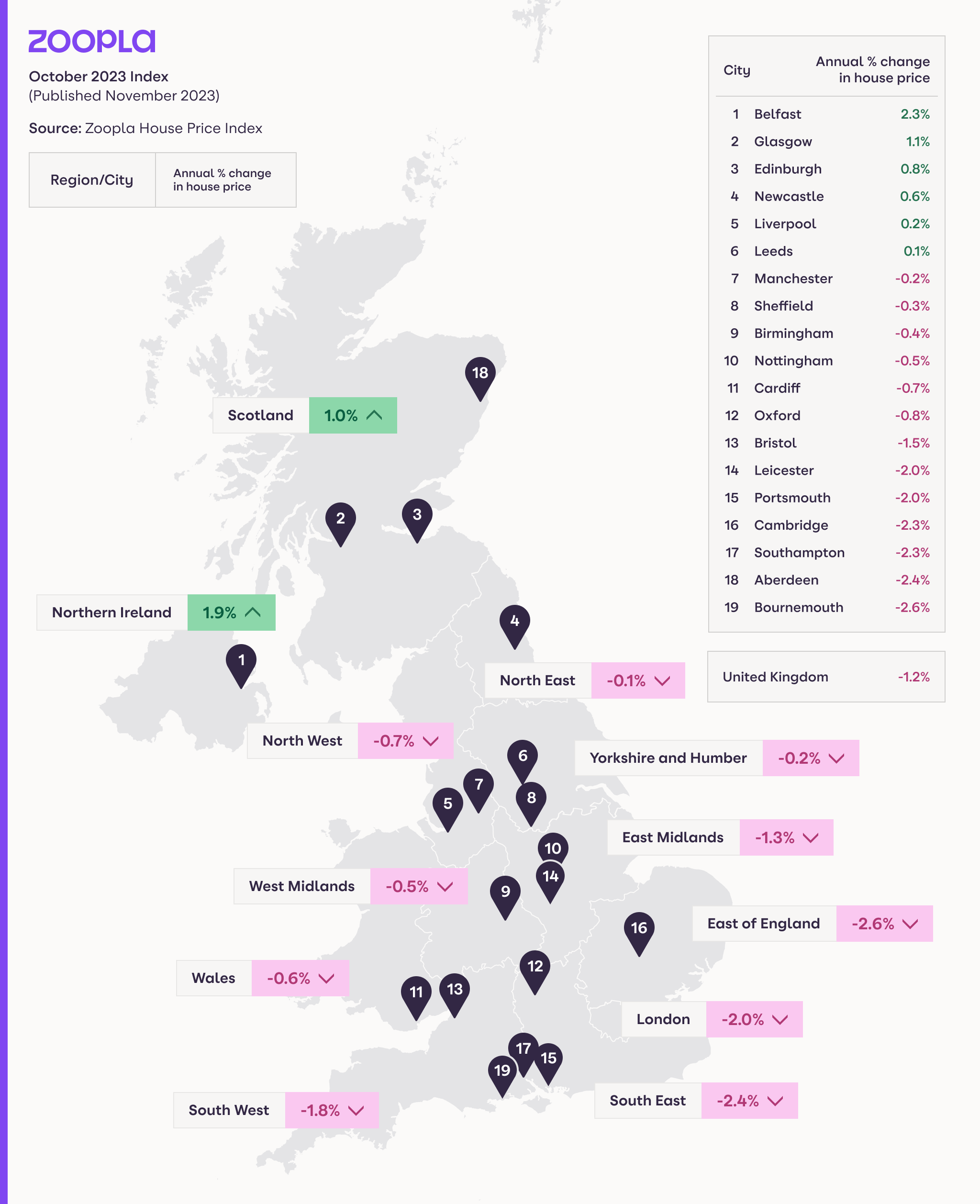

Sales are holding up across many parts of Scotland and have also picked up across inner London, where market activity has under- performed the rest of the UK over recent years. Overall, the market is on track for 1m sales completions in 2023 but the pipeline of deals as we approach the end of the year is the lowest for 4 years.