London and the East of England have led the rebound in new buyer demand in the first weeks of 2024. Most other areas recorded below-average increases in demand, typically rising in line with last year or only ahead by single digits.

The rebound in London is uniform across the market segments – inner- London, suburban outer-London and the core commuter areas around London. This could reflect a turn of fortunes for the London housing market. Over the last seven years, the city has lagged behind the rest of the UK in terms of sales volumes and house price inflation.

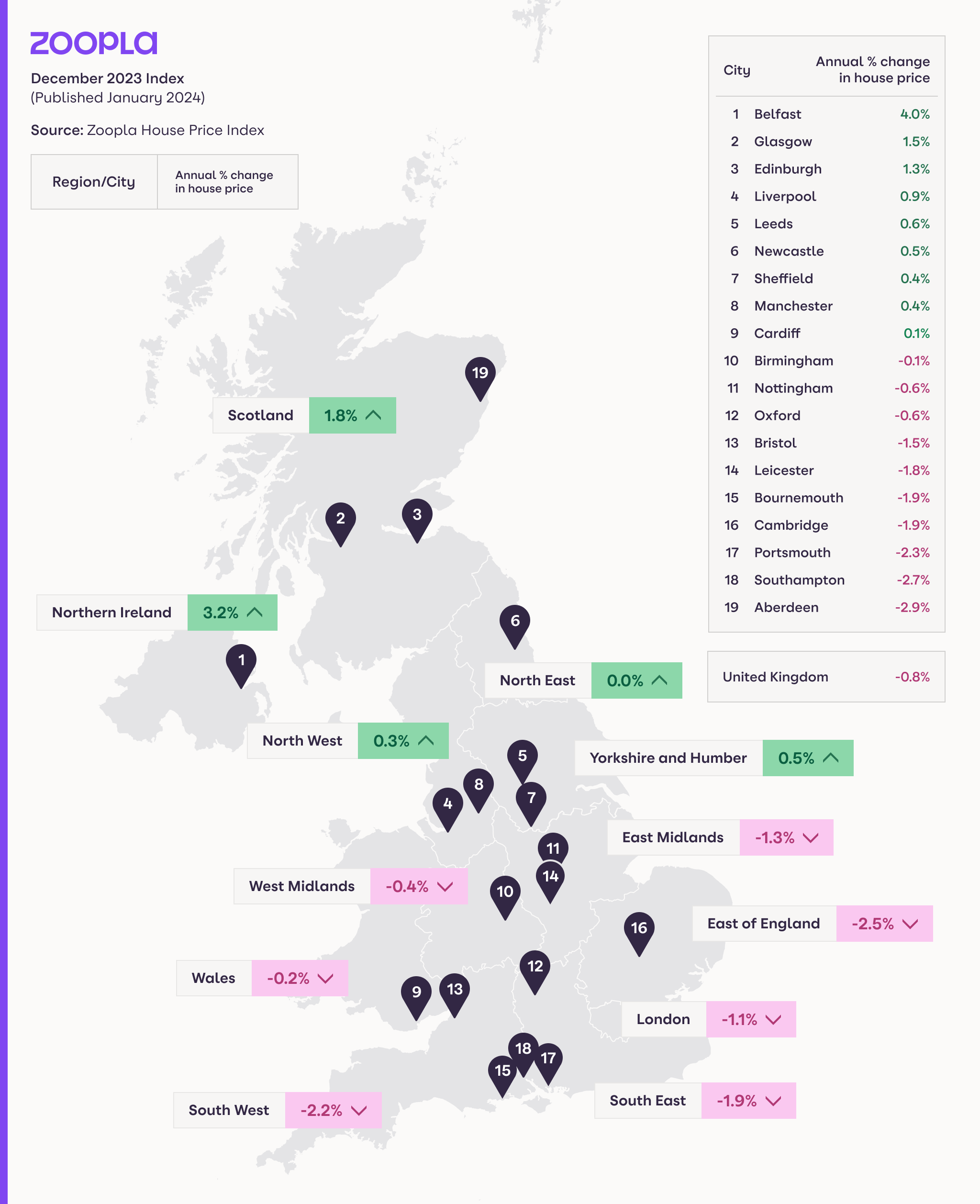

Our house price index shows that London house prices have risen just 13% since the start of 2016. Meanwhile, they are 34% higher across the UK and almost 50% higher in Wales. The average value of a flat in London is just 2% higher over the same period.

Fast house price appreciation in the early 2010’s saw London reach ‘peak unaffordability’ in 2016 with a price to earnings ratio of over 15x. A succession of factors has subsequently hit demand and pricing in the capital e.g. tax changes aimed at investors and overseas buyers, the Brexit vote, which hit jobs growth and a global pandemic that closed cities to travel and changed working patterns. This, combined with higher mortgage rates which have hit the most expensive housing markets hardest.

Low house price inflation since 2016 and rising earnings means housing affordability in London, measured on a house price to

earnings ratio basis, is at its lowest since 2014. However, London housing prices remain expensive by UK standards at 13x earnings.

Slowly improving housing affordability in London is positive news but home buyers still face a sizable affordability challenge with mortgage rates doubling since 2021. We expect market conditions in London to continue to improve over 2024, with earnings rising faster than house prices. This will continue to improve affordability and support levels of housing sales rather than boost house prices.