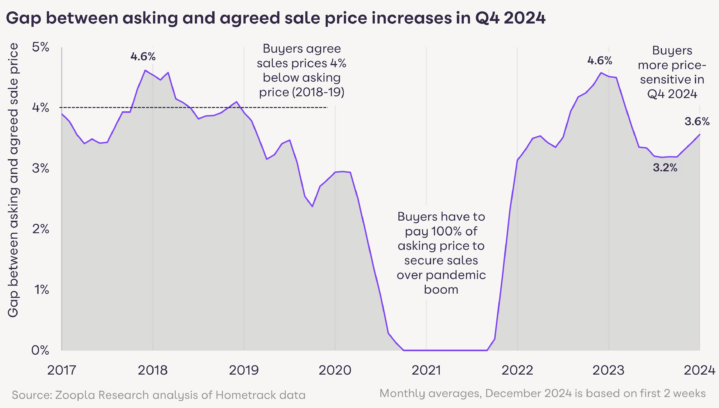

A leading indicator for house price inflation is the size of the gap between the asking price and the agreed sale price. The smaller the gap, the faster prices rise, while the larger the gap the slower prices rise (with the risk of price falls above a certain level).

The pre-pandemic (2018-2019) average sale was agreed at 4% below the asking price and annual house price growth averaged 2% a year. Over the pandemic boom, demand greatly exceeded supply and buyers had to pay 100% of the asking price or higher to secure a sale. UK house price inflation peaked at 10% in April 2022 as a result.

A buyer’s market returned over late 2022 and 2023 as mortgage rates spiked up to 5-6%. The gap between asking and sale prices peaked at 4.6% in late 2023, resulting in modest price falls. Market conditions improved over the first half of 2024 and buyers were willing to pay more of the asking price, resulting in a return to house price growth.

Buyers have become more price-sensitive in recent weeks in the wake of the Autumn Budget and amid growing uncertainty over the outlook for mortgage rates, which have drifted higher. Buyers are currently paying 3.6% below the asking price, compared to 3.2% over the summer, however it remains a buyer’s market. We expect a greater choice of homes for sale and price-sensitive buyers to continue to keep UK price inflation in check over 2025.